Invested into

Religare Health Trust 6 lots three weeks ago under my Cash portfolio and its share price did dip lower levels than the price which l have paid for it. Its share price improved in this week so l have divested all of it for a gain of $91.

Health care business is a good value investment. But the locations (Indonesia, India, Myanmar, etc.) in where a health care business is can be a great concern at times. Religare will be in my radar for re-investment when its share price goes lower levels again; and so are other health care related stocks in Singapore.

Under Cash portfolio this week l have invested into

GRP 15 lots. GRP recently invested into Australia gold mining company, Aphrodite Gold Limited. GRP will hold 12.7% equity interest in Aphrodite and the price paid was equivalent to AUD 6 cents per share. Aphrodite's last trading price on 9 Nov was at AUD 4.7 cents (52 weeks low 3.3 cents, 52 weeks high 9.48 cents). Gold mining is not GRP's core business which are marine and hoses, measuring instrument and PVC fittings but it has now becomes a new source of revenue for the company. GRP has strong balance sheet and healthy cash flow. GRP has been consistently paying 2 cents dividend in each year and at Friday's closing price $0.24 hence dividend yield is at 8.33%. Anyway, l am always ready to take profit first as l have divested all 15 lots

in the same week when its share price moved up; for a gain of $93. Likely to reinvest into GRP when its share price weakens.

Also this week under Cash portfolio, l have invested into

Keppel Reit 8 lots. Just like any other investments and divestments, l will not hesitate to letting it go when its share price in the coming week(s) improves. Otherwise l will be keeping it for passive income streams.

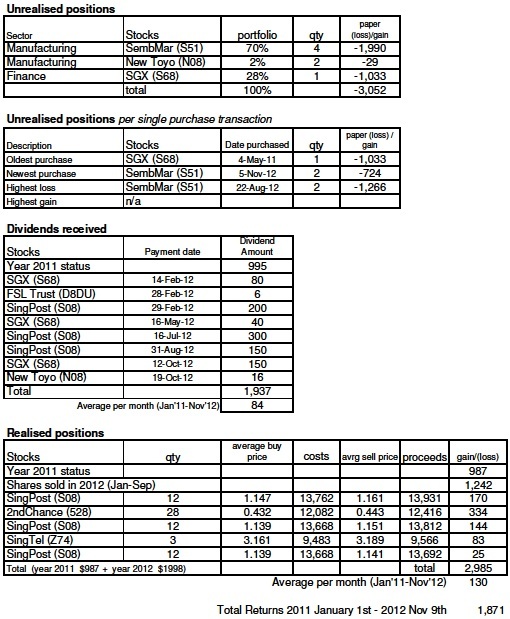

Portfolio walk since previous posting :-

-$364 Total Returns as of 2 Nov

+$184 Gains on sales of GRP and Religare

-$554 Unrealised positions worsened

-$734 Total Returns as of 9 Nov

previous posting :-

Cash - Closing Status 2 Nov