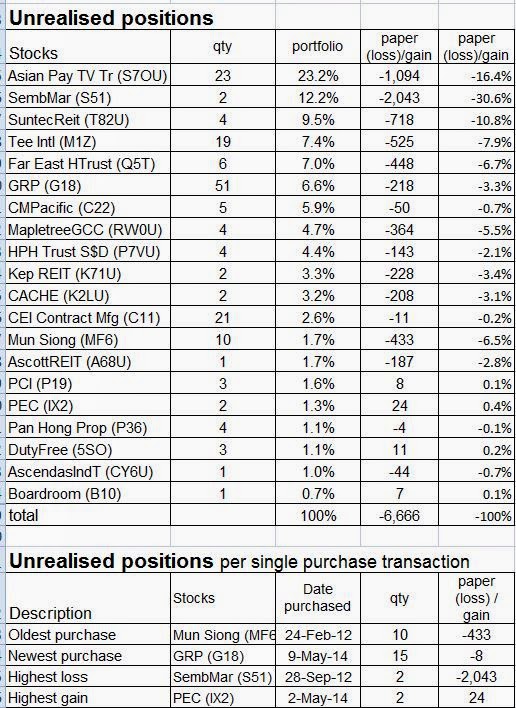

Divested away Croesus Retail Trust

3 lots in this week at breakeven as part of usual and active stock holdings re-balancing. For its 3Q2014 results, NPI

+12.3% and Income available for distribution per unit (SGD cents) +8.0%

versus Forecast. Higher NPI mainly due to better than expected tenant

sales at Mallage Shobu. Gearing 53.5%. Majority lease expiry by gross

rental income in FY2015 (21.5%) and FY2018 and beyond (67.5%). NAV as

of end Mar'14 at JPY 70.95 (SGD 0.87); friday close at $0.945.

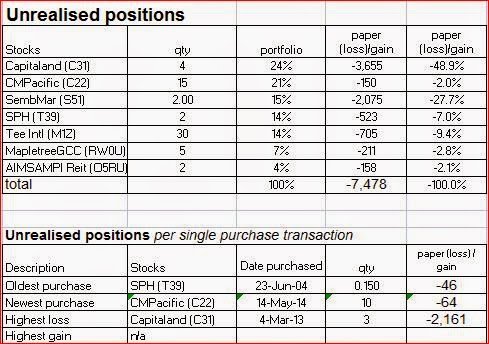

Divested away AIMS AMP Industrial Reit 2 lots in this week at breakeven as part of usual and active stock holdings re-balancing. In its 4Q2014 financial results, NPI +3.1%; available distributable income +6.5%. DPU -9.4%. Higher NPI due to lower expenditure incurred for its portfolio of properties. Lower DPU because of private placement in May 2013 and the recent rights issue in March 2014. Borrowing costs +S$1.4 million mainly due to the additional interest expense incurred on the AUD borrowings to fund the acquisition of 49.0% interest in Optus Centre which is located at Macquarie Park, Sydney, Australia. Earliest debt due for refinancing is in October 2015. Its NAV as of end Mar'14 was at $1.468 versus its last done share price on this Friday at $1.45. Portfolio occupancy rate at 97.0% as of end Mar'14. 72.1% of its borrowings on fixed rates taking into account the interest rate swaps and the Medium Term Notes. It also recently issued S$50 million 3.80% fixed rate notes due 2019. It had also recently received the Temporary Occupation Permit (TOP) for its redevelopment at 103 Defu Lane 10 on 28 May 2014. Next, it will undertake customized asset enhancement initiative (AEI) at 26 Tuas Avenue 7.

Divested away Keppel Reit 2 lots in this week at breakeven as part of usual and active stock holdings re-balancing. In its recent 1Q2014 financial results and versus last year; DPU stayed the same at 1.97 cents; Property expenses now stabilized at +4.3%; NPI higher by 14.7% resulted from improved performance from Ocean Financial Centre and Prudential Tower, as well as the additional income from 8 Exhibition Street in Melbourne; Profit +20.1% due to higher NPI, higher interest income, higher share of results of associates and jv, lower trust expenses and lower amortization expenses; but offset by lower rental support, higher borrowing costs and management fees as a results of the larger portfolio of assets under management. As of end Qtr 1, its NAV was valued at $1.39 but Mr Market believes that it is worth $1.305 as of its Friday closing price. Recently, it sold away 92.8% of its stake in Prudential Tower and the sale proceeds will be used to repay existing debt in order to achieve greater financial flexibility, with the remaining amount to be used for general corporate and working capital purposes and/or for pursuing acquisition opportunities. Post divestment, its aggregate leverage will decline from 42.1% to 38.8%.

SRS stock holdings walk since previous posting :-

SRS stock holdings walk since previous posting :-

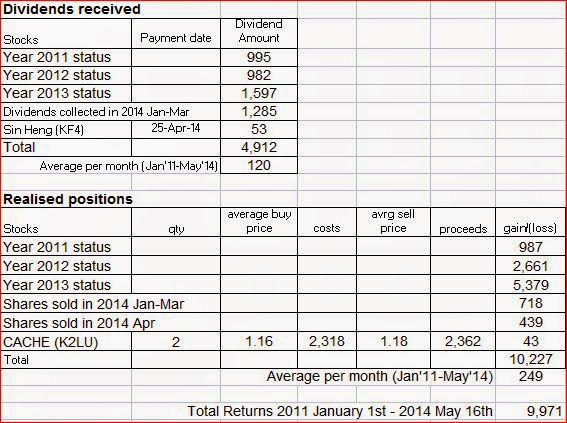

+$9,971 Total Returns as of 16 May

+$8 Nett gain on sales of Keppel Reit, Croesus Retail Trust, AIMS AMP Industrial Reit

-$343 Unrealised positions worsened

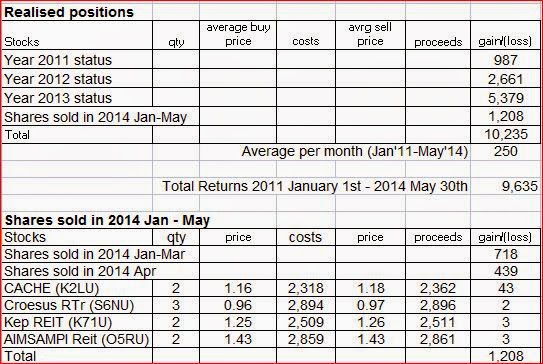

+$9,635 Total Returns as of 30 May

previous posting :- SRS - Closing status 16 May

Remarks :- Profits locked in to-date $15,148 / year 2014 $2,546

Divested away AIMS AMP Industrial Reit 2 lots in this week at breakeven as part of usual and active stock holdings re-balancing. In its 4Q2014 financial results, NPI +3.1%; available distributable income +6.5%. DPU -9.4%. Higher NPI due to lower expenditure incurred for its portfolio of properties. Lower DPU because of private placement in May 2013 and the recent rights issue in March 2014. Borrowing costs +S$1.4 million mainly due to the additional interest expense incurred on the AUD borrowings to fund the acquisition of 49.0% interest in Optus Centre which is located at Macquarie Park, Sydney, Australia. Earliest debt due for refinancing is in October 2015. Its NAV as of end Mar'14 was at $1.468 versus its last done share price on this Friday at $1.45. Portfolio occupancy rate at 97.0% as of end Mar'14. 72.1% of its borrowings on fixed rates taking into account the interest rate swaps and the Medium Term Notes. It also recently issued S$50 million 3.80% fixed rate notes due 2019. It had also recently received the Temporary Occupation Permit (TOP) for its redevelopment at 103 Defu Lane 10 on 28 May 2014. Next, it will undertake customized asset enhancement initiative (AEI) at 26 Tuas Avenue 7.

Divested away Keppel Reit 2 lots in this week at breakeven as part of usual and active stock holdings re-balancing. In its recent 1Q2014 financial results and versus last year; DPU stayed the same at 1.97 cents; Property expenses now stabilized at +4.3%; NPI higher by 14.7% resulted from improved performance from Ocean Financial Centre and Prudential Tower, as well as the additional income from 8 Exhibition Street in Melbourne; Profit +20.1% due to higher NPI, higher interest income, higher share of results of associates and jv, lower trust expenses and lower amortization expenses; but offset by lower rental support, higher borrowing costs and management fees as a results of the larger portfolio of assets under management. As of end Qtr 1, its NAV was valued at $1.39 but Mr Market believes that it is worth $1.305 as of its Friday closing price. Recently, it sold away 92.8% of its stake in Prudential Tower and the sale proceeds will be used to repay existing debt in order to achieve greater financial flexibility, with the remaining amount to be used for general corporate and working capital purposes and/or for pursuing acquisition opportunities. Post divestment, its aggregate leverage will decline from 42.1% to 38.8%.

+$9,971 Total Returns as of 16 May

+$8 Nett gain on sales of Keppel Reit, Croesus Retail Trust, AIMS AMP Industrial Reit

-$343 Unrealised positions worsened

+$9,635 Total Returns as of 30 May

previous posting :- SRS - Closing status 16 May

Remarks :- Profits locked in to-date $15,148 / year 2014 $2,546