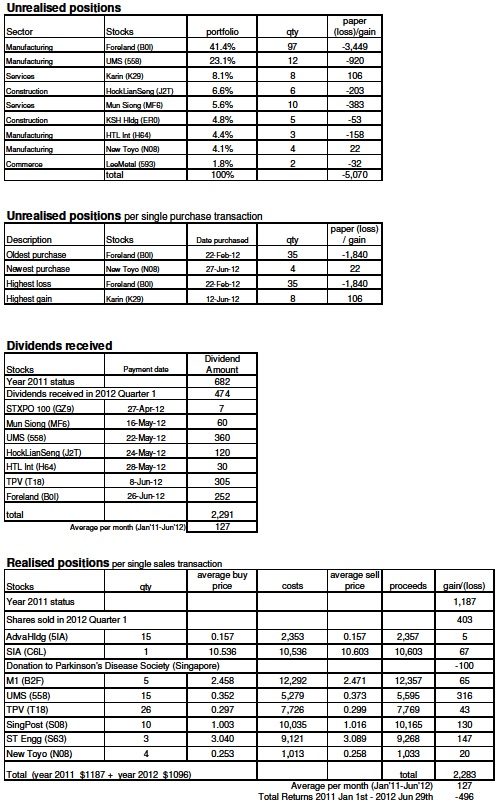

For the Cash portfolio this week, l have received a cheque in the mail on the dividends for Foreland Fabrictech. I am hoping for Foreland to improve on its share price and giving out higher dividends in the near future. Otherwise, l will need to find a way to reduce and eventually divest my investment in it.

Based on previous year, the next XD dividend date on ST Engineering is on 8 Aug at the rate of $0.03 and for my 3 lots investment in it then the projected dividends receivable is at $90. This week l have sold it all away so that l can receive its dividends in advance in the form of a disposal gain of $147.

Bought into New Toyo 8 lots this week but l have halved my investment in it within this week itself. The original plan was to divest the entire 8 lots because current price is already meeting my selling price target for an advance dividends. But unfortunately only managed to sell off 4 lots; which actually lowered the expected gain on the disposal because of inability to apportion out the brokerage charges on reduced number of shares sold. For next week, l will continue to divest the remaining 4 lots as l doubt current stock market bull run is sustainable and l am hoping to re-invest into it again at lower prices in the near future. l am attracted to New Toyo as it has gone through several management and operations makeovers in recent and past months. l reckon that all these makeovers at New Toyo were and are necessary in order for it constantly improving its operations efficiency and lowering running costs in the long run.

Portfolio walk since previous posting :-

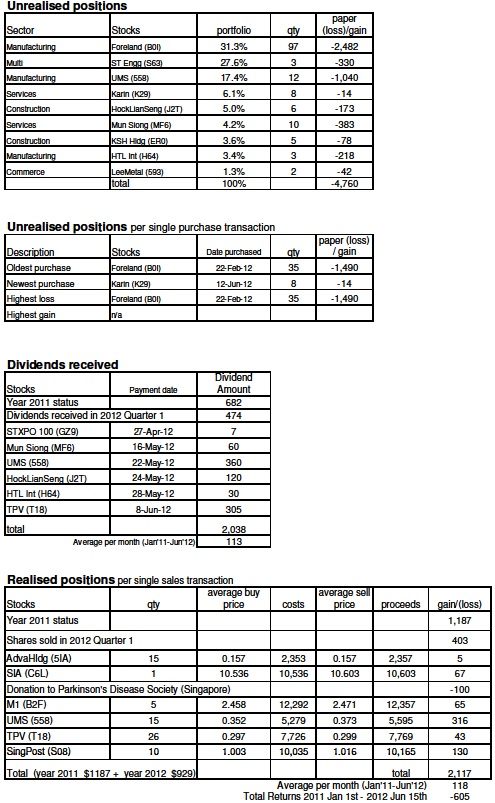

-$605 Total Returns as of 15 Jun

+$252 Dividends received from Foreland

+$167 Profits on sales of ST Engineering and New Toyo

-$310 Unrealised positions worsened

-$496 Total Returns as of 29 Jun

previous posting :- Cash - Closing Status 15 Jun

Based on previous year, the next XD dividend date on ST Engineering is on 8 Aug at the rate of $0.03 and for my 3 lots investment in it then the projected dividends receivable is at $90. This week l have sold it all away so that l can receive its dividends in advance in the form of a disposal gain of $147.

Bought into New Toyo 8 lots this week but l have halved my investment in it within this week itself. The original plan was to divest the entire 8 lots because current price is already meeting my selling price target for an advance dividends. But unfortunately only managed to sell off 4 lots; which actually lowered the expected gain on the disposal because of inability to apportion out the brokerage charges on reduced number of shares sold. For next week, l will continue to divest the remaining 4 lots as l doubt current stock market bull run is sustainable and l am hoping to re-invest into it again at lower prices in the near future. l am attracted to New Toyo as it has gone through several management and operations makeovers in recent and past months. l reckon that all these makeovers at New Toyo were and are necessary in order for it constantly improving its operations efficiency and lowering running costs in the long run.

Portfolio walk since previous posting :-

-$605 Total Returns as of 15 Jun

+$252 Dividends received from Foreland

+$167 Profits on sales of ST Engineering and New Toyo

-$310 Unrealised positions worsened

-$496 Total Returns as of 29 Jun

previous posting :- Cash - Closing Status 15 Jun